DELIVERIES of new containerships have hit 1.29 million TEU this year and will rise to 1.42 million TEU by January despite slackening demand on major trade lanes, according to the Paris-based consultancy Alphaliner.

More than 1.07 million TEU of new building capacity was delivered in 2009, falling short of the record 1.57 million TEU in 2008. Total capacity of the world's containership fleet is predicted to grow to 14.3 million TEU by January.

"Fleet capacity growth is expected to reach 9.5 per cent after taking into account the about 180,000 TEU deleted this year, both through scrapping and the removal of vessels from the cellular fleet following conversion for other uses," said Alphaliner.

"Some 276 containerships should be delivered this year, a figure comparable to the 268 units delivered in 2009. However, the average size of new ships has increased from last year's 3,990 TEU to 5,150 TEU in 2010.

"A record number of ships has been deferred or delayed over the past two years, due to the financial crisis. About 100 ships for 530,000 TEU delivered in 2010 were initially planned for delivery in 2009, while 65 ships for 435,000 TEU initially planned for delivery in 2010 have been deferred to 2011 and beyond.

"Net capacity growth is expected to reach 9.1 per cent next year, with 1.40 million TEU of new capacity due to hit the water," it said.

Since the start of the financial crisis, order cancellations or conversions of containership orders into other vessel types amounted to 530,000 TEU, or 7.9 per cent of the order book, at October 2008, according to Alphaliner records.

"The level of new deliveries is expected to remain close to 1.4 million TEU for each of the next two years. However, the size of new ships will rise significantly. The average size should reach 6,050 TEU for 2011 and 7,015 TEU for 2012 deliveries, as the number of new 10,000-TEU+ ships increases.

"Eight hundred and eight vessels above 10,000 TEU are expected to be delivered between now and the end of 2012, compared to 27 such units which have been delivered so far this year."

To highlight the most significant vessel deliveries so far this year, Geneva's MSC has taken in charge the MSC La Spezia from German owner Claus Peter Offen. It is the 16th unit in a programme of 26 ships of 13,798-14,000 TEU built by Samsung and DSME.

Vancouver's Seaspan Corporation has taken delivery of the Cosco Thailand, the sixth of eight ships of 8,495 TEU ordered by this owner in May 2007 from Hyundai Heavy Industries. The ship is scheduled to join Cosco's transpacific SEA service that it jointly operates with Hanjin.

Meanwhile, Hyundai Merchant Marine has taken in charge the Hyundai Vancouver, the last of five 6,350 TEU vessels chartered from UK-based Zodiac Maritime and built in Japan by the Imabari Group at its Koyo shipyard. This ship will join the New World Alliance's Far East-Europe Central China Express (CEX).

Japanese carrier "K" Line has taken delivery of the Brotonne Bridge, the first of five postpanamax ships of 4,520 TEU ordered from Samsung by non-operating owner Seaspan in November 2007. The Brotonne Bridge will be deployed on the CKYH PSW-1 service.

Alphaliner added that a further seven newbuildings of similar size are also being built at Hyundai Heavy Industries for "K" Line's own account. Four ships from this series have been delivered since May.

jueves, 28 de octubre de 2010

miércoles, 27 de octubre de 2010

Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 41, 2010)

This week, the China export containerized transport market showed marginally sagged as the capacity increasingly swelled over the demand, pulling down the freight rate of most main services.

On October 15th, the China (Export) Containerized Freight Index issued by the Shanghai Shipping Exchange reported 1,153.17 points, down 3.7% from last week; while the Shanghai (Export) Containerized Freight Index quoted 1,301.31 points, down 5.4% from last week.

In Europe service, the slightly decreasing cargo volume affected the slot utilization. The freight rate showed a downward trajectory and averaged at USD 1,500-1,600/TEU. As for the Mediterranean service, the cargo volume was even less, and the freight rate dipped to USD 1,550/TEU. Pundits expected that the slump trend would prevail over the next few months due to the Christmas goods shipment rush had finished before the National Day of China while the capacity was still at a high level. Therefore, capacity surplus is expected to continue and will consequently trigger people's bearish sentiment for the next 3 months. On October 15th, the freight indices of Europe and Mediterranean services issued by the SSE reported 1,681.56 points and 1,752.35 points, respectively dived by 4.5% and 4.8% from last week.

The North America trade encountered a similar situation of the Europe market, where the cargo volume kept shrinking while the capacity remained ample. Although the cancellation of some voyages from Shanghai to US led to a few full-filled ships during the National Day holiday, still the slots remained quite spare as the slot utilization hovered around 80% this week. With signs of a downward cargo volume after the end of the Christmas goods shipment rush, most insiders hold a downbeat attitude to the market until the end of 2010. On October 15th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in US west coast and US east coast issued by the SSE were USD 2,379/FEU and USD 3,797/FEU, respectively tumbled by 4.6% and 4.1% from last week.

The cargo volume kept stable in Australia and Singapore service, but the freight rate only stood at about USD 1,000/TEU because of the weakening market condition. Christmas goods are still being carried, which is expected to last to November, since the route is far shorter than those to Europe and U.S. On October 15th, the freight rate (ocean freight plus surcharges) from Shanghai to base ports of the Australia and Singapore service issued by the SSE stood at USD 1,003/TEU, with a week-on-week decrease of 4.1%.

In Southeast Asia service, the cargo volume slightly decreased, yet the freight rate showed relatively steady, as it had already dropped before the National Day holiday. On October 15th, the freight index of the Southeast Asia service issued by the SSE reported 974.64 points, basically equal to last week.

The slot utilization for the voyages from Shanghai to Japan service descended to 65% this week, a sharp declined compared to last week, nevertheless, the freight rate remained firm. On October 15th, the freight index of the Japan service issued by the SSE reported 749.18 points, almost no change from last week.

This week, the China export containerized transport market showed marginally sagged as the capacity increasingly swelled over the demand, pulling down the freight rate of most main services.

On October 15th, the China (Export) Containerized Freight Index issued by the Shanghai Shipping Exchange reported 1,153.17 points, down 3.7% from last week; while the Shanghai (Export) Containerized Freight Index quoted 1,301.31 points, down 5.4% from last week.

In Europe service, the slightly decreasing cargo volume affected the slot utilization. The freight rate showed a downward trajectory and averaged at USD 1,500-1,600/TEU. As for the Mediterranean service, the cargo volume was even less, and the freight rate dipped to USD 1,550/TEU. Pundits expected that the slump trend would prevail over the next few months due to the Christmas goods shipment rush had finished before the National Day of China while the capacity was still at a high level. Therefore, capacity surplus is expected to continue and will consequently trigger people's bearish sentiment for the next 3 months. On October 15th, the freight indices of Europe and Mediterranean services issued by the SSE reported 1,681.56 points and 1,752.35 points, respectively dived by 4.5% and 4.8% from last week.

The North America trade encountered a similar situation of the Europe market, where the cargo volume kept shrinking while the capacity remained ample. Although the cancellation of some voyages from Shanghai to US led to a few full-filled ships during the National Day holiday, still the slots remained quite spare as the slot utilization hovered around 80% this week. With signs of a downward cargo volume after the end of the Christmas goods shipment rush, most insiders hold a downbeat attitude to the market until the end of 2010. On October 15th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in US west coast and US east coast issued by the SSE were USD 2,379/FEU and USD 3,797/FEU, respectively tumbled by 4.6% and 4.1% from last week.

The cargo volume kept stable in Australia and Singapore service, but the freight rate only stood at about USD 1,000/TEU because of the weakening market condition. Christmas goods are still being carried, which is expected to last to November, since the route is far shorter than those to Europe and U.S. On October 15th, the freight rate (ocean freight plus surcharges) from Shanghai to base ports of the Australia and Singapore service issued by the SSE stood at USD 1,003/TEU, with a week-on-week decrease of 4.1%.

In Southeast Asia service, the cargo volume slightly decreased, yet the freight rate showed relatively steady, as it had already dropped before the National Day holiday. On October 15th, the freight index of the Southeast Asia service issued by the SSE reported 974.64 points, basically equal to last week.

The slot utilization for the voyages from Shanghai to Japan service descended to 65% this week, a sharp declined compared to last week, nevertheless, the freight rate remained firm. On October 15th, the freight index of the Japan service issued by the SSE reported 749.18 points, almost no change from last week.

Rotterdam Containers Jump 17 Percent

Europe's top container hub on track to match record volume of 2008

Oct 22. -- Container traffic in Rotterdam increased 17 percent in the first nine months of 2010 from a year ago to 8.4 million 20-foot equivalent units, putting Europe's top container hub on track to match the record volume of 2008.

Rotterdam slightly increased its lead over its closest rival Antwerp, which boosted container traffic 16.9 percent in the first three quarters of the year to 6.3 million TEUs.

Rotterdam's total throughput increased 13.4 percent to 321 million metric tons as almost all cargo sectors posted growth, led by a 112 percent surge in iron ore and scrap shipments to 31 million metric tons and a 31 percent rise in other dry bulk traffic to 9 million metric tons.

"The growth is leveling off, but is still slightly higher than expected," said Hans Smits, Chief Executive of the Port of Rotterdam Authority.

"The port continues to profit from strong European exports, for which a lot of raw materials also need to be imported," Smits said.

"Total throughput is now exactly at the 2008 level … it is exciting to see whether or not we will succeed in climbing out of a deep trough to achieve a record in just one year."

Rotterdam handled a record 421 million metric tons in 2008 with container shipments hitting an all time high of 10.8 million TEUs.

Roll-on, roll-off traffic increased 6 percent in the first nine months to 13 million metric tons driven by the tentative recovery of the British economy. Growth could increase further in the fourth quarter due partly to the deployment of larger vessels, the port said.

Breakbulk and general cargo traffic recovered 14 percent to 5 million metric tons of steel, paper products, fruit, metals and project cargo.

Oct 22. -- Container traffic in Rotterdam increased 17 percent in the first nine months of 2010 from a year ago to 8.4 million 20-foot equivalent units, putting Europe's top container hub on track to match the record volume of 2008.

Rotterdam slightly increased its lead over its closest rival Antwerp, which boosted container traffic 16.9 percent in the first three quarters of the year to 6.3 million TEUs.

Rotterdam's total throughput increased 13.4 percent to 321 million metric tons as almost all cargo sectors posted growth, led by a 112 percent surge in iron ore and scrap shipments to 31 million metric tons and a 31 percent rise in other dry bulk traffic to 9 million metric tons.

"The growth is leveling off, but is still slightly higher than expected," said Hans Smits, Chief Executive of the Port of Rotterdam Authority.

"The port continues to profit from strong European exports, for which a lot of raw materials also need to be imported," Smits said.

"Total throughput is now exactly at the 2008 level … it is exciting to see whether or not we will succeed in climbing out of a deep trough to achieve a record in just one year."

Rotterdam handled a record 421 million metric tons in 2008 with container shipments hitting an all time high of 10.8 million TEUs.

Roll-on, roll-off traffic increased 6 percent in the first nine months to 13 million metric tons driven by the tentative recovery of the British economy. Growth could increase further in the fourth quarter due partly to the deployment of larger vessels, the port said.

Breakbulk and general cargo traffic recovered 14 percent to 5 million metric tons of steel, paper products, fruit, metals and project cargo.

138 ships idle, rising 2pc to 289,000 TEU as peak passes

THE idle containership fleet grew two per cent to 138 ships, or 289,000 TEU, compared to 132 ships of 243,000 TEU, two weeks ago, reported the Paris-based consultancy Alphaliner.

Four recently idled ships are above 7,500 TEU, the first of that size to fall into unemployment as the annual slack season began.

To avoid lay-ups, Cosco assigned its surplus 8,500-TEU newbuilding, the COSCO Thailand, to the South China Express, a Far East-US west coast string it operates with Hanjin, linking Fuzhou, Nansha, Hong Kong, Shenzhen-Yantian, Xiamen, Long Beach and Oakland, as an additional ship.

This inclusion stretches the rotation by from 35 to 42 days through the application of extra slow steaming. The transit time is extended westbound, extra slow steaming from Oakland to Nansha on the west side of the Pearl north of Shenzhen.

APL will deploy its surplus ships to a new China-Indonesia loop mid-November, prompted by higher China volumes to ASEAN, making them the largest containerships to call at Indonesian ports.

APL's China Indonesia Service (CIS) will link Shanghai, Ningbo, Xiamen, Shenzhen-Chiwan, Singapore, Jakarta, Surabaya, Jakarta, Singapore, Laem Chabang and back to Shanghai.

CIS will include four ships in the 2,400 to 3,500 TEU range, the APL Sydney, APL Minneapolis, the APL Bangkok and the APL Pusan with the first sailing of the APL Sydney from Shanghai on November 15.

Three of the four ships have been reassigned from the Far East-US west coast loops where they were sent as peak season loaders.

CIS service complements the Korea China Straits (KCS) service launched by APL in July 2009, and links the Pearl River Delta and Jakarta. The KCS calls at Busan, Kaohsiung, Hong Kong, Nansha, Shenzhen-Chiwan, Port Kelang, Singapore, Jakarta, Singapore, Kaohsiung, Taipei, Lianyungang and back to Busan deploying four ships in the 2,400 to 3,500 TEU range. These ships are the largest vessels to call at the Indonesian ports.

The new CIS service encompasses APL's Singapore-Jakarta-Surabaya feeder loop and serves also the Thailand market on the northbound leg to China.

Fifty-six per cent of the Far East-US west coast services have adopted extra slow steaming, and this is expected to grow as more ships become idle, said Alphaliner.

But even with full adoption of extra slow steaming, additional transpacific capacity limits will only be able to absorb 110,000 TEU, not enough to utilise what tonnage will become available in coming months, said the report.

Four recently idled ships are above 7,500 TEU, the first of that size to fall into unemployment as the annual slack season began.

To avoid lay-ups, Cosco assigned its surplus 8,500-TEU newbuilding, the COSCO Thailand, to the South China Express, a Far East-US west coast string it operates with Hanjin, linking Fuzhou, Nansha, Hong Kong, Shenzhen-Yantian, Xiamen, Long Beach and Oakland, as an additional ship.

This inclusion stretches the rotation by from 35 to 42 days through the application of extra slow steaming. The transit time is extended westbound, extra slow steaming from Oakland to Nansha on the west side of the Pearl north of Shenzhen.

APL will deploy its surplus ships to a new China-Indonesia loop mid-November, prompted by higher China volumes to ASEAN, making them the largest containerships to call at Indonesian ports.

APL's China Indonesia Service (CIS) will link Shanghai, Ningbo, Xiamen, Shenzhen-Chiwan, Singapore, Jakarta, Surabaya, Jakarta, Singapore, Laem Chabang and back to Shanghai.

CIS will include four ships in the 2,400 to 3,500 TEU range, the APL Sydney, APL Minneapolis, the APL Bangkok and the APL Pusan with the first sailing of the APL Sydney from Shanghai on November 15.

Three of the four ships have been reassigned from the Far East-US west coast loops where they were sent as peak season loaders.

CIS service complements the Korea China Straits (KCS) service launched by APL in July 2009, and links the Pearl River Delta and Jakarta. The KCS calls at Busan, Kaohsiung, Hong Kong, Nansha, Shenzhen-Chiwan, Port Kelang, Singapore, Jakarta, Singapore, Kaohsiung, Taipei, Lianyungang and back to Busan deploying four ships in the 2,400 to 3,500 TEU range. These ships are the largest vessels to call at the Indonesian ports.

The new CIS service encompasses APL's Singapore-Jakarta-Surabaya feeder loop and serves also the Thailand market on the northbound leg to China.

Fifty-six per cent of the Far East-US west coast services have adopted extra slow steaming, and this is expected to grow as more ships become idle, said Alphaliner.

But even with full adoption of extra slow steaming, additional transpacific capacity limits will only be able to absorb 110,000 TEU, not enough to utilise what tonnage will become available in coming months, said the report.

martes, 19 de octubre de 2010

CMA CGM to sell 20pc of itself to Turks for US$500 million

MARSEILLES' CMA CGM, the third largest carrier in the world, is close to accepting the deal of selling 20 per cent of its shares to Turkish group Yildirim for US$500 million.

If CMA CGM agrees the offered term, it will receive payment at the end of November, said French financial daily Les Echos, and the French government's strategic investment fund, FSI, is expected to invest in CMA CGM after signing the agreement, according to seatradeasia-online.com.

This French-based shipping line has suffered from considerable debt, which is said amounting to $5 billion, after the global recession, and been keen to look for new investors since, according to London's International Freighting Weekly.

If CMA CGM agrees the offered term, it will receive payment at the end of November, said French financial daily Les Echos, and the French government's strategic investment fund, FSI, is expected to invest in CMA CGM after signing the agreement, according to seatradeasia-online.com.

This French-based shipping line has suffered from considerable debt, which is said amounting to $5 billion, after the global recession, and been keen to look for new investors since, according to London's International Freighting Weekly.

LA and Long Beach post substantial gains in September

THE ports of Los Angeles and Long Beach continued to show a year-on-year September volume increases, but container throughput growth has slowed since August, tonnage statistics show.

The Port of Los Angeles handled 711,613 TEU, 22 per cent more than a year earlier. "Overall it's been a very strong year, better than we forecast, but not completely unexpected given the declines of 2009," said an LA port spokesman. "Consumer demand in the months head remains relatively uncertain."

Long Beach moved 30.5 per cent more boxes in September at 574,790 TEU up from 440,364 TEU in the same month in 2009. Year to date, the port container volume was up 12.4 per cent to 5,936,066 TEU up from the 5,282,385 moved in the first nine months of 2009.

Long Beach import and export containers though Long Beach port increased 30.5 per cent in September year on year, but that was off six per cent from August. Loaded import containers in September increased year on year 28 per cent to 288,905 TEU from 224,929 TEU last year. Year to date, volume has increased 14.2 per cent to 2,982,320 TEU from 2,612,227 TEU.

Loaded export containers at Long Beach in September increased 13 per cent to 124,021 TEU from 109,337 TEU year to date laden outbound boxes increased 11.5 per cent to 1,484,610 TEU from 1,331,872 TEU.

Movement of empties increased 52.6 per cent to 161,864 106 TEU from 103 in September at Long Beach with a total year-to-date tally of 1,469,136 TEU up from 1,338,286 TEU, an increase of 9.8 per cent.

The Port of Los Angeles handled 711,613 TEU, 22 per cent more than a year earlier. "Overall it's been a very strong year, better than we forecast, but not completely unexpected given the declines of 2009," said an LA port spokesman. "Consumer demand in the months head remains relatively uncertain."

Long Beach moved 30.5 per cent more boxes in September at 574,790 TEU up from 440,364 TEU in the same month in 2009. Year to date, the port container volume was up 12.4 per cent to 5,936,066 TEU up from the 5,282,385 moved in the first nine months of 2009.

Long Beach import and export containers though Long Beach port increased 30.5 per cent in September year on year, but that was off six per cent from August. Loaded import containers in September increased year on year 28 per cent to 288,905 TEU from 224,929 TEU last year. Year to date, volume has increased 14.2 per cent to 2,982,320 TEU from 2,612,227 TEU.

Loaded export containers at Long Beach in September increased 13 per cent to 124,021 TEU from 109,337 TEU year to date laden outbound boxes increased 11.5 per cent to 1,484,610 TEU from 1,331,872 TEU.

Movement of empties increased 52.6 per cent to 161,864 106 TEU from 103 in September at Long Beach with a total year-to-date tally of 1,469,136 TEU up from 1,338,286 TEU, an increase of 9.8 per cent.

HK up 4.9pc in September to 1.9 million TEU, Singapore rises 4.1pc

FIGURES from the Hong Kong Marine Department show the port handled 1.9 million TEU in September, an increase of 4.9 per cent over the 1.8 million TEU in September of last year.

Singapore's Maritime and Port Authority reported a 4.1 per cent increase in container movement in September, having handled 2.2 million TEU compared to 2.1 million TEU in September of last year.

Singapore's Maritime and Port Authority reported a 4.1 per cent increase in container movement in September, having handled 2.2 million TEU compared to 2.1 million TEU in September of last year.

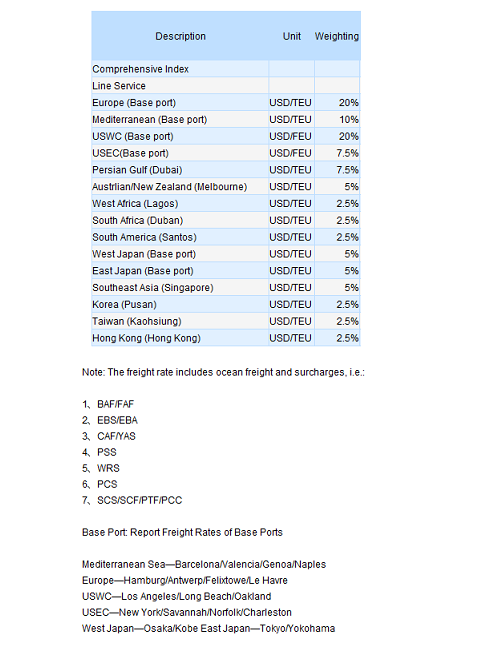

Tianjin Shipping Index makes debut

TIANJIN International Trade and Shipping Service Centre recently released the Tianjin Shipping Index (TSI), a comprehensive index reflecting the fluctuation of the northern China shipping market, Xinhua reported.

TSI is jointly developed by the Tianjin International Trade and Shipping Service Centre, Tianjin Port Group and Nankai University. TSI will initially include the Tianjin Container Freight Index (TCI) and the Tianjin Bulk Freight Index (TBI), which tracks shipping rates and indicate supply-demand relation in north China market.

The TCI index selects 14 shipping lanes as samples. These lanes cover Europe, the Mediterranean, America, south east Asia and the Persian Gulf.

The TBI index reflect the rise and fall of shipping rates of bulk cargo such as coal, ore and grain. It selects 10 shipping lanes as samples that cover major grain producing areas in North and South America.

The Tianjin International Trade and Shipping Service Centre releases the TCI index at 10am and the TBI index at 3pm every business day.

TSI is jointly developed by the Tianjin International Trade and Shipping Service Centre, Tianjin Port Group and Nankai University. TSI will initially include the Tianjin Container Freight Index (TCI) and the Tianjin Bulk Freight Index (TBI), which tracks shipping rates and indicate supply-demand relation in north China market.

The TCI index selects 14 shipping lanes as samples. These lanes cover Europe, the Mediterranean, America, south east Asia and the Persian Gulf.

The TBI index reflect the rise and fall of shipping rates of bulk cargo such as coal, ore and grain. It selects 10 shipping lanes as samples that cover major grain producing areas in North and South America.

The Tianjin International Trade and Shipping Service Centre releases the TCI index at 10am and the TBI index at 3pm every business day.

martes, 5 de octubre de 2010

According to the most recently publicized Circular of General Administration Office of State Council on Arrangement of Holidays in 2010, the dates of SCFI publication in 2010 are as follows (totally 48 issues):

Jan.: 8th, 15th, 22nd, 29th

Feb.: 5th, 12th, 26th

Mar.: 5th, 12th, 19th, 26th

Apr.: 2nd, 9th, 16th, 23rd, 30th

May: 7th, 14th, 21st, 28th

Jun.: 4th, 11th, 18th, 25th

Jul.: 2nd, 9th, 16th, 23rd, 30th

Aug.: 6th, 13th, 20th, 27th

Sep.: 3rd, 10th, 17th

Oct.: 15th, 22nd, 29th

Nov.: 5th, 12th, 19th, 26th

Dec.: 3rd, 10th, 17th, 24th, 31st

Jan.: 8th, 15th, 22nd, 29th

Feb.: 5th, 12th, 26th

Mar.: 5th, 12th, 19th, 26th

Apr.: 2nd, 9th, 16th, 23rd, 30th

May: 7th, 14th, 21st, 28th

Jun.: 4th, 11th, 18th, 25th

Jul.: 2nd, 9th, 16th, 23rd, 30th

Aug.: 6th, 13th, 20th, 27th

Sep.: 3rd, 10th, 17th

Oct.: 15th, 22nd, 29th

Nov.: 5th, 12th, 19th, 26th

Dec.: 3rd, 10th, 17th, 24th, 31st

Suscribirse a:

Comentarios (Atom)