Jan 4 -- The top 20 container lines increased their operated capacity 14 percent over the last 12 months, as the strong recovery in freight volume led carriers to take on new tonnage over 2010, Alphaliner reported.

Jan 4 -- The top 20 container lines increased their operated capacity 14 percent over the last 12 months, as the strong recovery in freight volume led carriers to take on new tonnage over 2010, Alphaliner reported.

The total liner capacity of both cellular and non-cellular vessels grew 8.6 percent in 2010 to reach 14.8 million 20-foot equivalent units as of Jan. 1, 2011, according to the Paris-based information service.

The total cellular fleet stands at 4,849 ships with a nominal capacity of 14,270,000 TEUs, up 9.1 percent from January, 2010.

The total capacity of the fleet operated by the top 20 carriers reached 12.3 million TEUs compared to 10.8 million TEUs a year ago.

The overall share of the top 20 carriers as a percentage of the global liner fleet rose to 83 percent from 79 percent, as the large carriers’ capacity additions outpaced the overall increase in liner capacity.

Over the last year, the top 20 carriers have reduced their idled capacity from 740,000 TEUs, or 6.9 percent of their operated capacity as of Jan. 1, 2010 to only 136,000 TEUs currently, or 1.1 percent of their operated fleet.

Eighteen of the top 20 carriers increased their operated capacity, with only NYK and “K” Line logging a decline in the last 12 months, Alphaliner said.

Mediterranean Shipping Co., the second largest container line, recorded the largest increase in capacity over the last 12 months, adding 375,000 TEUs to its fleet, up 25 percent.

In relative terms, the strongest capacity increase was made by CSAV with a 74 percent growth in the last 12 months from 333,000 TEUs to 579,000 TEUs currently, Alphaliner said.

By contrast, the capacity of Maersk Line, the world’s largest carrier, increased a modest 5 percent in the 12-month period, while that of Evergreen, the fourth-largest carrier grew 8 percent.

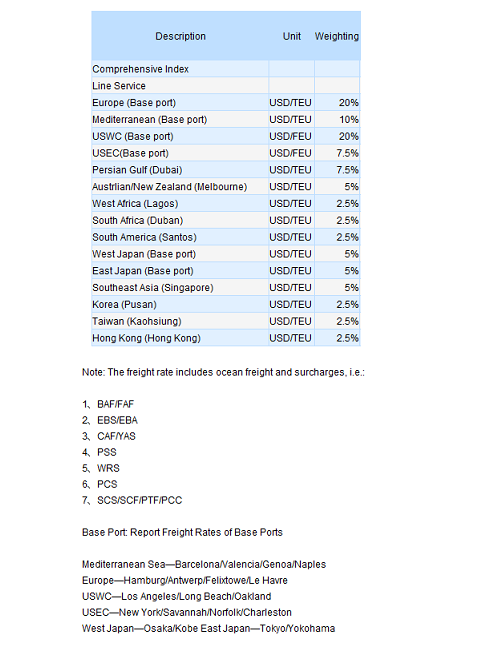

Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 05, 2011)

This week, the demand of the China containerized transport market was warmed by the shipment rush ahead of the Conventional Spring Festival, where the cargo volume boosted evidently on services like Europe and North America, nevertheless, the increase of which seemed not strong enough due to the excessive capacity. On January 21st, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1060.64 points; while the Shanghai Containerized Freight Index came out at 1107.85 points, both declined 0.4% from last week.

Stepping into the peak period of the cargo exporting before the Spring Festival, the Europe service was seen its shipment volume keeping thriving and the slot utilization jumped to 95%, besides, fright rate remained steady. On January 21st, the freight index of the Europe service issued by SSE was 1482.37 points, basically no change with last week. In spite of the current prosperous market, cargo volume will definitely turn dull once entering the festival, until then there will be capacity cutting policies like voyages readjustment and cancellation on most services. As a result, how cargo volume recovers afterwards turn out to be the key of the short-term market. Freight rate will incur significant downward pressure if the cargo volume behaves with a disappointing growth by the moment.

In North America service, the market showed no signs of improvement because of the swelling capacity, although the cargo volume rose steadily. Slot utilization stayed around 90%. Statistics from CI ONLINE indicated a 1.723m TEU of capacity was engaging from Far-east to US west coast as of January 1st, multiplying by 48000TEU from December 2010. Bearish sentiments of the short-term market left carriers cutting the price for solicitation, where the restoration of the freight rate has been offsetting mostly by its downward trajectory since early January.

n January 21st, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in US west coast and US east coast services were USD 1955/FEU and USD 3168/FEU, respectively down 1.1% and 0.9% from last week.

Still, thanks to the pre-Spring Festival, both the transport demand and the cargo volume in Australia and Singapore service showed upward momentum. Also, the recent appreciating exchange rate of the Australian dollar against RMB greatly enhanced the purchasing power of the consignees in acceptance places, propelling the increase of the cargo volume. Besides, the sharp contract of the capacity on the service since late January pulled the slot utilization up to above 95% this week, where laden vessels and steady freight rate could be witnessed as consequence.

In Japan service, cargo volume marginally ascended and the slot utilization hovered around 70%, and freight rate maintained steady as usual. On January 21st, the freight index of the Japan service reported 753.40 points, generally remained the same from last week.

Latest report from Alphaliner informs that the growth of this year’s containerized transport market will back to normal, which the cargo volume is estimated to perk up by 7.7% annually. However the global capacity will be expected to inflate as well, by 1.3m TEU, or 8.6% from 2010, darkening the market of 2011.

Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 02, 2011)

This week, the demand of China’s containerized transport market saw upward, as the strong shipment on the Europe and America services curbed the slumping freight rate. On 2010 December 31st, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1053.93 points, almost no change with last week; while the Shanghai Containerized Freight Index reported 1122.68 points, with an week-on-week increase of 3.7%.

Europe service entered its annual final stage this week, where the cargo volume sharply raised, pushing the slot utilization to 100%; whereas Mediterranean service was relatively weaker than the Europe service as the growth of the shipment exporting to North Africa showed lackluster, but still the cargo volume kept the rising trajectory with the slot utilization having climbed to 95%. Some of the carriers managed to restore the freight rate on January 1st 2011, bounding up the price of slot reservation for the first time after the 10 Q4. On December 31st, the freight rates (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Europe and Mediterranean services nailed at USD 1401/TEU and USD 1250/TEU, respectively up 4.4% and 1.2%.

In North America service, the cargo volume kept the mounting momentum and sustained the slot utilization to above 95%. Considering the growing cargo volume, carriers were poised to upraise the freight rate, and some of them had already done that. On 2010 December 31st, the freight rates (ocean freight plus surcharges) for the voyages from Shanghai to base ports in US east coast and US west coast quoted USD 1962/FEU and USD 3169/FEU, both of which increased more than USD 100/FEU. Seasonal factors substantially boosted the demand of the capacity. The indices, however, which demonstrate the US economic consuming power was quite mixed, with the December retail sales increased and consumer confidence index dropped compared to the previous month. As a result, the short-term market on the North America service remains unclear. Besides, it was rumored that carriers drastically diverged about the range of the peak season surcharge, ranging from USD 200/FEU ~ USD 400/TEU. Moreover, some of them probably delay the PPS to 2011 January 15th.

The prevailing rate restoration on the main west-east services like Europe and Mediterranean had encouraged most carriers on other services to follow the step, where several liner operators announced to hike the rate with various degrees in January on West Africa, South Africa and Persian Gulf services.

In Australia and Singapore services the cargo volume showed steady, so did the freight rate, where the slot utilization for most voyages averaged about 90%. With the huge capacity and the limited cargo resources mostly emerging on the service over the past year, the surplus capacity seems hopeless to alleviate, so people are cautious about next year. Recently, members of the Asia Australia Discussion Agreement announced to gradually cut the capacity on the Far East/Australia service since the end of January to June. Such extensive and durative adjustment may widely influent next year’s market, as some carriers had declared to uplift the freight rate at January 15th by about USD 250/TEU.

On Japan service, the cargo volume were perceived obviously sluggish, for the figure shrunk by 30% from last week and the slot utilization saw no more than 50%. On December 31st, the freight index of the Japan service issued by SSE reported 739.38 points.

EUROPEAN container volumes strengthened last year with January to November imports up 15.4 per cent over 2009, while exports rose 10.3 per cent.

Container Trade Statistics (CTS) data showed that exports from Europe to Asia increased 3.6 per cent to 463,600 TEU in November, up from 447,600 TEU in October, reported London's International Freighting Weekly. European imports from Asia in November totalled 1.1 million TEU, up one per cent on October.

But exports from north Europe to Asia declined in November for a third month, and were 12.5 per cent down on August's peak for 2010, said the report, adding that rates on the trade continued to soften in November, for a fourth month.NNNN

1/10/11 Freight Rates Tumbling as 35-Mile Line of Ships Sails Even at an average of $22,000, ship owners should be able to make money, with average daily expenses last year of about $15,000 for costs including crew and depreciation, Clarkson estimates. While the figure doesn’t include payments on loans, interest rates for many companies have dropped since the Federal Reserve cut its benchmark interest rate to near zero in December 2008 and kept it there since. Bloomberg

BUNKER SURCHARGE (BS)

Further to our announcement dated November 24, 2010, it is noted that the following BSs apply effective January 15, 2011 as follows:-

January 15, 2011 December 15, 2010

WCSA/WCCA USD774TEU USD738TEU

Mexico USD548/TEU USD522/TEU

The foregoing adjustment will be done by individual Members at their discretions on voluntary and non-binding basis.

December 24, 2010. Secretary.