CONTAINERSHIP deliveries are expected to reach a record high of two million TEU in 2013, according to a recent report by maritime analyst, Alphaliner, which if accurate could signal a significant oversupply problem on the horizon.

According to Alphaliner's figures, new vessel orders for delivery in 2013 have increased from 0.38 million TEU to 1.59 million TEU in the last 12 months, exceeding the 1.57 million TEU in 2008.

New orders have also outpaced deliveries in the past 12 months.

Alphaliner's data shows that a total of 222 containerships, not including undeclared options, have been ordered, while containership deliveries reached 214 units…

"With all 2011 and most of 2012 delivery slots currently booked, attention now turns to 2013 slots. Scheduled deliveries for 2013 have surged from 380,000 TEU a year ago to 1.59 million TEU today, and there is still available shipyard capacity for 2013 deliveries. If all current options, letters of intent (LOI) and intended orders were exercised, 2013 vessel deliveries could exceed two million TEU," Alphaliner said.

The new orders bring the capacity growth forecast for 2013 to 8.9 per cent, which is expected to increase further to 11.3 per cent if options and LOIs are added.

Besides, shipowners have placed orders for a total of 1.6 million TEU of new capacity since June 2010, surpassing deliveries recorded in the same period that hit 1.4 million TEU.

Since January 2010, a total of 1.58 million TEU of new containerships have been ordered. Of those newly ordered vessels, carriers' orders account for 67 per cent or 1.06 million TEU, while orders from non-operating owners (NOO) account for the rest of the 30 per cent or 0.52 million TEU, Alphaliner said.

Overall, Alphaliner's figures reveal that the total investments in new containerships since January 2010 have swollen to US$18.8 billion.

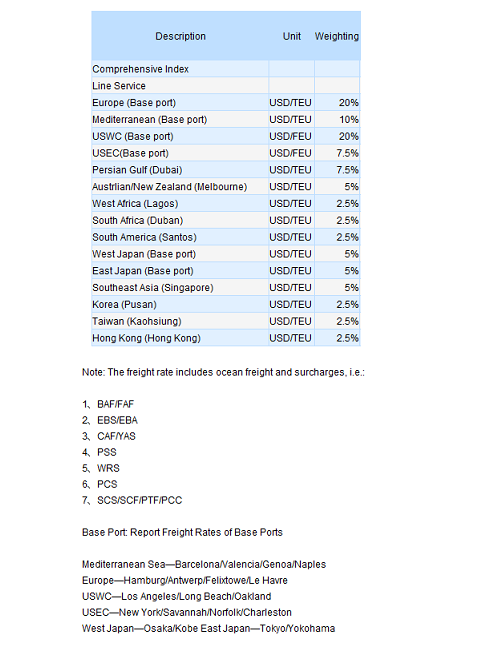

Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 21, 2011)

This week, the China containerized transport market remained sound, with a stable comprehensive index. On May 20th, the China Containerized Freight Index issued by Shanghai Shipping Exchange was 1013.37 points; while the Shanghai Containerized Freight Index came out at 1075.60 points, both hardly changed from last week.

In Europe service, the cargo volume stood still and the slot utilization averaged at 90%. Besides, some carriers continued reducing the freight rate, as on May 20th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Europe was USD 892/TEU, down 1.8% from last week. While the Europe service was perceived calm, the cargo volume in Mediterranean was relatively prosperous. Meanwhile, carriers’ previously prudent control over the capacity had gradually worked, making the slots become so insufficient that the utilization ratio reached above 95%, and laden voyages were seen as well. The apparent amelioration between supply and demand had effectively curbed and marginally upturned the freight rate’s downward trend. On May 20th, the freight rate (ocean freight plus surcharges) of the voyages exporting to the Mediterranean service quoted USD 924/TEU, which is USD 32/TEU higher than the Europe service. Industrial insiders opined that the approaching conventional peak season on the service could propel the steady rising momentum of the freight rate. Some carriers had claimed to impose a peak season surcharge, at about USD 200/TEU, on early June.

In North America service, the cargo volume of US west coast saw slightly soared, where the slot utilization kept hovering around 90%. While in US east coast, however, the unchanged over-supply kept pressuring on the freight rate, which dropped more than USD 100/FEU in some voyages. On May 20th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to US west coast and Us east coast services were USD 1819/FEU and USD 3188/FEU, respectively slipped 1.2% and 0.9% from last week.

In Australia and Singapore service, despite the constant increase in the cargo volume after May, yet since such increase didn’t meet the market expectation, the supply-demand relation was still losing the balance, and the slot utilization had decreased to 80%. The freight rate kept falling as well. On May 20th, the freight index of the Australia and Singapore service reported 962.73 points, down 1.0% from last week. It was rumored that some carriers were poised to add capacity on the service after June, which is very likely to contribute to the capacity surplus and cool down the freight rate.

In Persian Gulf service this week, the shipment rush ahead of the Ramadan steadily pushed up the cargo volume, where the slot utilization showed above 95% and some voyages reported out of slots. On May 20th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Persian Gulf service was USD 1001/TEU, up 5.8% from last week.

In Japan service, the cargo volume kept hiking as end of May is coming, where the slot utilization climbed over 70% and the freight rate maintained firmly. On May 20th, the freight index of the Japan service issued by SSE came out at 824.36 points.