(CCFI Commentary in Issue 44, 2010)

This week, the China’s export containerized transport market showed slightly sluggish, as freight rates in most services kept falling, especially in North America. On November 5th, the China (Export) Containerized Freight Index issued by Shanghai Shipping Exchange reported 1118.70 points; while the Shanghai (Export) Containerized Freight Index was 1242.87 points, both of which reduced 1.3% from last week.

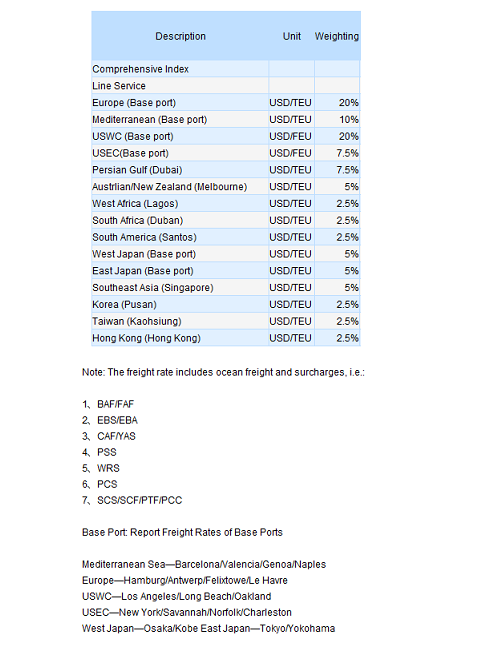

There was a slightly descend of the cargo volume in Europe service this week, yet still the slot utilization was witnessed above 90% and some of the voyages reported laden. The rate continued the downward momentum, with a drop range at about USD 25/TEU ~ USD 50/TEU due to the overwhelming capacity. In Mediterranean service the rate was understood even lower, for the rates in some of the voyages were cut to USD 1300/TEU, and the general freight rate remained at USD 1400/TEU ~ USD 1500/TEU. On November 5th, the freight indices of Europe and Mediterranean services issued by Shanghai Shipping Exchange reported 1609.40 points and 1678.65 points, respectively slip 0.8% and 0.5% from last week. Some of the carriers indicated that they were prepare to laid part of the vessels on the Europe and Mediterranean service to stabilized the freight rate if it keeps slipping because of the surplus capacity.

In North America service the cargo volume carried on the contraction trend, and the capacity increasingly exceeded the demand. Consequently the decline in the freight rate intended to enlarge, where on US west coast this week the rate averaged at USD 2100/FEU ~ USD 2200/FEU, while in US east coast service the figure showed USD 3400/FEU ~ USD 3500/FEU. On November 5th, the freight rates (ocean freight plus surcharges) for the voyages from Shanghai to base ports in US west coast and US east coast quoted USD 2159/FEU and USD 3459/FEU, respectively down 2.0% and 2.8%. According to experts, quite substantially had the rate shifted on the America service. Both the plummet of the USDX and the new currency quantitative easing policy announced by the US Federal Reserve will to some extend curb the growth of US general imports, and consequently inflict the freight rate on America service.

In Australia and Singapore service, both the cargo volume and the freight rate remained strong because of the Christmas shipments, where generally the rate for the service averaged at about USD 1100/TEU, up by about USD 50/TEU from last week. On November 5th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Australia and Singapore service was seen USD 1099/USD, up 4.5% from last week. Pundits believe the Christmas shipments will end in early December, and some of the carriers are poised to cut the capacity by then to maintain the current rate level.

On Japan service, the average slot utilization, just as last week, was seen above 80%, while the freight rate remained steady. On November 5th, the freight index of the Japan service issued by Shanghai Shipping Exchange showed 760.10 points, basically equaling to last week.

In Southeast Asia service this week the cargo volume slightly slid down and the freight rate kept the downward trajectory. The freight rate (without surcharges) for the voyages from Shanghai to base ports in Singapore, marginally went down from last week, dropping to USD 110/TEU ~ USD 150/TEU. On November 5th, the freight index of the Southeast Asia service issued by Shanghai Shipping Exchange reported 924.33 points, down 1.4% from last week.

No hay comentarios:

Publicar un comentario