Posted by FT Alphaville on Feb 24 11:22.

Hitting the wires at pixel time — an astonishing promise:

RIYADH, Feb 24 (Reuters) – Saudi Arabia is willing and able to supply high quality, light oil to replace any lost Libyan crude, senior Saudi sources said on Thursday.

“Saudi is willing and capable of supplying oil of the same quality, either Arab extra light or through blending,” one source said…

Some West African crude, such as Angolan crude can also be redirected to Europe, the sources said, while Saudi Arabia could temporarily send extra oil to Asia to compensate.

Well, the feasibility of a straight Libyan-Saudi swap has been an issue. Needless to say, prices of Arab Light and Arab Extra Light have been spiking sharply higher following the chaos in Libyan production:

This, though, appears to be offering a complicated, global swap of oil products — one which leaves Saudi Arabia relatively exposed to the market’s current gyrations. For one thing, blending means that they would need ready access to condensates and other components. It’s also by no means easy to create a perfect substitute, even with blending.

Meanwhile, it’s also worth noting that Saudi Aramco announced only days ago that it would become active in the swaps market — a move which has reportedly been in the pipeline for some time:

Aramco, one of the largest exporters of fuel oil and naphtha into East Asia as well as a net importer of gas oil, is also expected to make its debut in the oil swaps market when it starts trading, traders said…

Aramco, which had already started optimising production for the past one to two years, is expected to trade conservatively in the swaps market, mainly for hedging purposes and not be seen as engaging in market-moving trading plays, the traders added.

This could prove useful for hedging any unanticipated basis risk brought about crude differential exposure.

A bit like the central bank of oil opening itself up for a swap line arrangement — but in a scenario in which Saudi Arabia becomes the equivalent of the Fed, with a euro shortage problem.

Although there is one fly in the ointment, however — unrest hitting Saudi itself. Protests are currently scheduled for a ‘Day of Rage’ on March 11, although it’s a fast-changing situation as eyes flash from Tripoli — to Riyadh.

By Joseph Cotterill and Izabella Kaminska

lunes, 28 de febrero de 2011

China's 2010 gross oceanic product reaches 3.8 trillion yuan

Feb.28--The State Oceanic Administration (SOA) told Xinhua Saturday that China's gross oceanic product was worth 3.8 trillion yuan (577.89 billion U.S. dollars). The figure accounted for 9.7 percent of the nation's total gross domestic product in 2010 and 16 percent of the GDP in coastal areas. China's gross oceanic product surged from 1.77 trillion yuan in 2005 to 3.8 trillion yuan last year, an annual increase of 13.5 percent, said the SOA. In the past five years, the oceanic industry provided 33 million jobs to people in the coastal areas.

(Source:Xinhua)

(Source:Xinhua)

Container shipping volumes to rise 10pc in 2011: SeaAxis

Feb.28--PARIS based SeaAxis, the container leasing arm of Axis Intermodal UK, forecasts that demand for container shipping services will rise more than 10 per cent this year on the back of a recovery in the global economy led by the strength of emerging nations. On the other hand, its quarterly report on box shipping also predicts that overall freight rates will fall by another 10 per cent in the second quarter, reports Newark's Journal of Commerce. The biggest threat to the ocean liner industry is overcapacity, which "will peak soon before diminishing later this year as trade volume rises," the report said."The highest risks facing the container shipping industry at this time, in order of importance, are: acceleration of redeployment of vessel capacity, increase in fuel costs, increase in container prices, commodity price surge and regional political instability, said SeaAxis vice president Philippe Hoehlinger.But he remained optimistic. "The underlying fundamentals for container shipping remain largely favourable in the mid-term with the forging of global supply chains, the rise in merchandise trade and the emergence of BRIC countries still creating demand for the future."

(Source:Shippingazette)

(Source:Shippingazette)

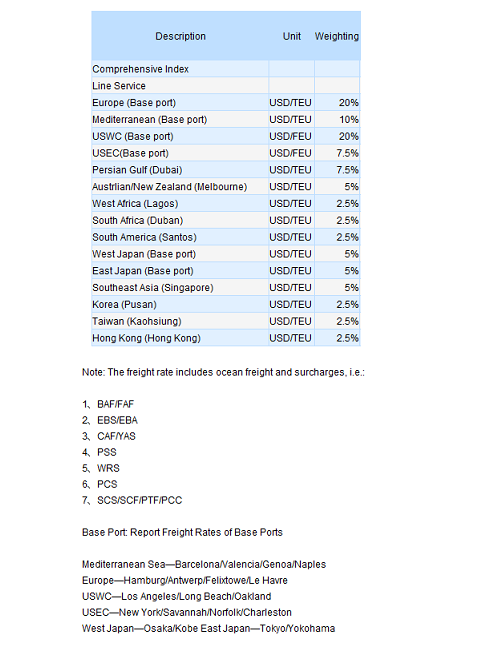

CCFI Commentary Issue 08, 2011

Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 08, 2011)

On February 18th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1052.52 points, basically the same from last week; while the Shanghai Containerized Freight Index came out at 1060.47 points, down 2.8% from last week.

In Europe service the shipment was so weak that the slot utilization only showed 80% even carriers attempted to uplift the freight rate with capacity cutting, voyage suspending, and slow steaming. Unfortunately, the result was disappointing. On February 18th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Europe quoted USD 1246/TEU, slipped by 4.5% from last week. Commentaries from the insiders indicated the China's export was basically entangled by the post Chinese new year effect which have yet to fade since part of the plants still haven't resumed production completely, also, the slow production cycle of some of the manufactures contributes as well.

In North America service the cargo volume kept shrinking this week as the slot utilization dropped to 70%, while the freight rate tended to decline even tougher. On February 18th, the freight rate (ocean freight plus surcharges) of the voyages to base ports in US west coast and US east coast were USD 1835/TEU and USD 3056/TEU, respectively down 3.4% and 2.2% from last week. What's worth mentioning is the optimism of US federal reserve board, who predicted the economic growth for 2011 at 3.4% ~ 3.9%, up by 0.4% compared to the figure previously announced in 2010 November. Should the over-estimated growth come real, the prosperity of North America service will be greatly driven forward.

In Singapore and Australia service the cargo volume preserved the downward trajectory as the slot utilization hold below 50%. On February 18th, the freight rate (ocean freight plus surcharges) to the base ports in Australia and Singapore services saw USD 820/TEU, slid 4.5% from last week. With the significant amount of fleet deployed last year, the glut of capacity hardly changed although carriers had put efforts to ameliorate the situation. Under the current downward pressure of the shipment, carriers are now commonly conservative about the short-term market.

Shipments in Japan service turned thriving, but no stronger than half of it was before the holiday. And the freight rate remained hard to rally because of the doom expectations for the next month. On February 18th, the freight index of the Japan service reported 749.37 points, marginally descended from last week.

In Southeast Asia service both the cargo volume and the freight rate slumped, as on February 18th, the freight rate (ocean freight plus surcharges) from Shanghai to Southeast Asia showed USD 149/TEU, down 2.6% from last week. Latest statistics in January from China customs informed that the bilateral trade with ASEAN Free Trade Area has outdo that of with Japan and became the third greatest trading partner for China. Thanks to the sound establishment of ASEAN Free Trade Area, the rapid growing strength of the shipment on the Southeast Asia services would be regarded as one of the most powerful engine for the China's transport market when most western services appeared stagnant.

(CCFI Commentary in Issue 08, 2011)

On February 18th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1052.52 points, basically the same from last week; while the Shanghai Containerized Freight Index came out at 1060.47 points, down 2.8% from last week.

In Europe service the shipment was so weak that the slot utilization only showed 80% even carriers attempted to uplift the freight rate with capacity cutting, voyage suspending, and slow steaming. Unfortunately, the result was disappointing. On February 18th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Europe quoted USD 1246/TEU, slipped by 4.5% from last week. Commentaries from the insiders indicated the China's export was basically entangled by the post Chinese new year effect which have yet to fade since part of the plants still haven't resumed production completely, also, the slow production cycle of some of the manufactures contributes as well.

In North America service the cargo volume kept shrinking this week as the slot utilization dropped to 70%, while the freight rate tended to decline even tougher. On February 18th, the freight rate (ocean freight plus surcharges) of the voyages to base ports in US west coast and US east coast were USD 1835/TEU and USD 3056/TEU, respectively down 3.4% and 2.2% from last week. What's worth mentioning is the optimism of US federal reserve board, who predicted the economic growth for 2011 at 3.4% ~ 3.9%, up by 0.4% compared to the figure previously announced in 2010 November. Should the over-estimated growth come real, the prosperity of North America service will be greatly driven forward.

In Singapore and Australia service the cargo volume preserved the downward trajectory as the slot utilization hold below 50%. On February 18th, the freight rate (ocean freight plus surcharges) to the base ports in Australia and Singapore services saw USD 820/TEU, slid 4.5% from last week. With the significant amount of fleet deployed last year, the glut of capacity hardly changed although carriers had put efforts to ameliorate the situation. Under the current downward pressure of the shipment, carriers are now commonly conservative about the short-term market.

Shipments in Japan service turned thriving, but no stronger than half of it was before the holiday. And the freight rate remained hard to rally because of the doom expectations for the next month. On February 18th, the freight index of the Japan service reported 749.37 points, marginally descended from last week.

In Southeast Asia service both the cargo volume and the freight rate slumped, as on February 18th, the freight rate (ocean freight plus surcharges) from Shanghai to Southeast Asia showed USD 149/TEU, down 2.6% from last week. Latest statistics in January from China customs informed that the bilateral trade with ASEAN Free Trade Area has outdo that of with Japan and became the third greatest trading partner for China. Thanks to the sound establishment of ASEAN Free Trade Area, the rapid growing strength of the shipment on the Southeast Asia services would be regarded as one of the most powerful engine for the China's transport market when most western services appeared stagnant.

lunes, 21 de febrero de 2011

Maersk Reported In $2 Billion Order for 18,000-TEU Ships

Deal with Daewoo Shipbuilding for 10 ships could double, Reuters reports

Feb.21--A.P. Moller-Maersk placed a $2 billion order for 10 18,000 20-foot equivalent unit container ships with South Korea’s Daewoo Shipbuilding and Marine Engineering, according to published reports, setting a new standard in the rapid escalation in vessel capacity.

The parent of Maersk Line, the world’s largest container ship operator, also is negotiating options for another 10 vessels of the same size, which would take the total value of the contract to $4 billion, according to a report by Reuters out of Hong Kong.

“The deal has been signed and they are preparing details ahead of a public announcement expected next week,” Reuters quoted an unnamed source as saying.

A.P. Moller-Maersk played down the report. “We do not comment on rumors and we have not signed any deal with Daewoo,” a spokesman for the Copenhagen-based company said.

Maersk Line’s North Asia chief executive, Tim Smith, has scheduled a news conference for Monday in Hong Kong to outline the carrier’s plans for Asia.

Reports that Maersk was planning to order ships with almost 4,000 TEUs more capacity than the current largest vessels first surfaced in November.

The Danish carrier launched the era of super-sized container vessels in 2006 with the launch of the Emma Maersk, the first of eight sisterships, whose capacity was officially declared to be 12,500 TEUs but was widely believed to be closer to 14,000 TEUs.

Feb.21--A.P. Moller-Maersk placed a $2 billion order for 10 18,000 20-foot equivalent unit container ships with South Korea’s Daewoo Shipbuilding and Marine Engineering, according to published reports, setting a new standard in the rapid escalation in vessel capacity.

The parent of Maersk Line, the world’s largest container ship operator, also is negotiating options for another 10 vessels of the same size, which would take the total value of the contract to $4 billion, according to a report by Reuters out of Hong Kong.

“The deal has been signed and they are preparing details ahead of a public announcement expected next week,” Reuters quoted an unnamed source as saying.

A.P. Moller-Maersk played down the report. “We do not comment on rumors and we have not signed any deal with Daewoo,” a spokesman for the Copenhagen-based company said.

Maersk Line’s North Asia chief executive, Tim Smith, has scheduled a news conference for Monday in Hong Kong to outline the carrier’s plans for Asia.

Reports that Maersk was planning to order ships with almost 4,000 TEUs more capacity than the current largest vessels first surfaced in November.

The Danish carrier launched the era of super-sized container vessels in 2006 with the launch of the Emma Maersk, the first of eight sisterships, whose capacity was officially declared to be 12,500 TEUs but was widely believed to be closer to 14,000 TEUs.

Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 07, 2011)

This week, the China containerized transport market turned gloomy under the post-Chinese lunar new year, as both cargo volume and freight rates shrunk apparently in most main services.

On February 11th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1051.14 points, down 0.8% from last week; while the Shanghai Containerized Freight Index came out at 1091.33 points, down 1.2% from last week.

In Europe service, cargo volume fell drastically comparing to the period before the lunar new year, but with the support of the carrier’s capacity readjustment the slot utilization maintained at 85% while the freight rate descended a little.

On February 11th, the freight index of the Europe service issued by SSE reported 1453.65 points, down 1.3% from last week.

Pundits believed the downward trajectory of the general market hardly changed since it was still in its slack season, but an upsurging momentum is expected to rise after Arpil according to the empirical evidence, which would probably buoyed the container market.

In North America services the sharp decrease in cargo volume this week pulled down the slot utilization to about 80%. And the current sluggish market was mainly shaped by two reasons, first of which is the substantially slumped shipment caused by most manufacturers’ shutdown during the lunar new year; while the second is that the shipment rush ahead of the holiday had fore-delivered part of the cargos in this week, leaving carriers no choice but declining freight rate for solicitation.

On February 11th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in US west coast and US east coast quoted USD 1900/FEU and USD 3124/FEU, respectively down 1.7% and 1.3%.

The cargo volume had greatly contracted on the Australia service after the holiday whereas the freight rate slightly slid a little. While the impact from the flood eased gradually, carriers have been stingy with the capacity since late January, however, the fact of the prevailing slack season and the abundant stockpile had significantly depress the import, lowering the demand of capacity as consequence.

On February 11th, the freight rate (ocean freight plus surcharges) of the voyages to the base ports in Australia and Singapore services saw USD 859/TEU, down 1% from last week.

In Japan service, the slot utilization dropped terribly to less than 50%, while the freight rate maintained steady.

On February 11th, the freight index of the Japan service was 764.68 points, barely changed from last week.

Latest statistics from Japan’s Ministry of Finance showed that the total trade between Japan and China has reached 26.5 trillion yen, up 22.3% from last year, almost returning to the record high before the crisis.

This week, the China containerized transport market turned gloomy under the post-Chinese lunar new year, as both cargo volume and freight rates shrunk apparently in most main services.

On February 11th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1051.14 points, down 0.8% from last week; while the Shanghai Containerized Freight Index came out at 1091.33 points, down 1.2% from last week.

In Europe service, cargo volume fell drastically comparing to the period before the lunar new year, but with the support of the carrier’s capacity readjustment the slot utilization maintained at 85% while the freight rate descended a little.

On February 11th, the freight index of the Europe service issued by SSE reported 1453.65 points, down 1.3% from last week.

Pundits believed the downward trajectory of the general market hardly changed since it was still in its slack season, but an upsurging momentum is expected to rise after Arpil according to the empirical evidence, which would probably buoyed the container market.

In North America services the sharp decrease in cargo volume this week pulled down the slot utilization to about 80%. And the current sluggish market was mainly shaped by two reasons, first of which is the substantially slumped shipment caused by most manufacturers’ shutdown during the lunar new year; while the second is that the shipment rush ahead of the holiday had fore-delivered part of the cargos in this week, leaving carriers no choice but declining freight rate for solicitation.

On February 11th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in US west coast and US east coast quoted USD 1900/FEU and USD 3124/FEU, respectively down 1.7% and 1.3%.

The cargo volume had greatly contracted on the Australia service after the holiday whereas the freight rate slightly slid a little. While the impact from the flood eased gradually, carriers have been stingy with the capacity since late January, however, the fact of the prevailing slack season and the abundant stockpile had significantly depress the import, lowering the demand of capacity as consequence.

On February 11th, the freight rate (ocean freight plus surcharges) of the voyages to the base ports in Australia and Singapore services saw USD 859/TEU, down 1% from last week.

In Japan service, the slot utilization dropped terribly to less than 50%, while the freight rate maintained steady.

On February 11th, the freight index of the Japan service was 764.68 points, barely changed from last week.

Latest statistics from Japan’s Ministry of Finance showed that the total trade between Japan and China has reached 26.5 trillion yen, up 22.3% from last year, almost returning to the record high before the crisis.

jueves, 3 de febrero de 2011

Suscribirse a:

Comentarios (Atom)