Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 08, 2011)

On February 18th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1052.52 points, basically the same from last week; while the Shanghai Containerized Freight Index came out at 1060.47 points, down 2.8% from last week.

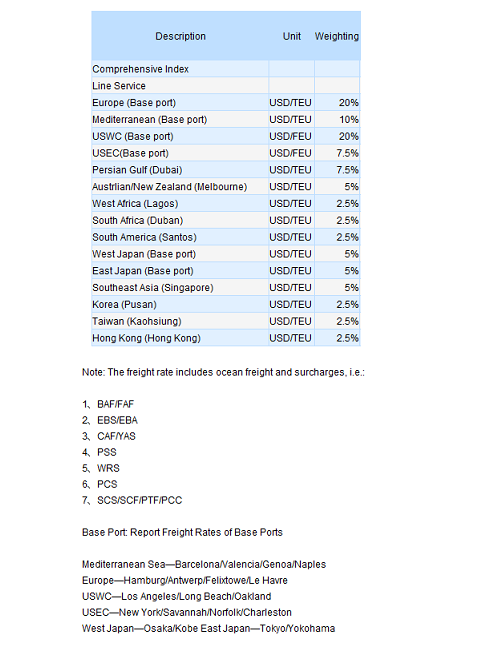

In Europe service the shipment was so weak that the slot utilization only showed 80% even carriers attempted to uplift the freight rate with capacity cutting, voyage suspending, and slow steaming. Unfortunately, the result was disappointing. On February 18th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Europe quoted USD 1246/TEU, slipped by 4.5% from last week. Commentaries from the insiders indicated the China's export was basically entangled by the post Chinese new year effect which have yet to fade since part of the plants still haven't resumed production completely, also, the slow production cycle of some of the manufactures contributes as well.

In North America service the cargo volume kept shrinking this week as the slot utilization dropped to 70%, while the freight rate tended to decline even tougher. On February 18th, the freight rate (ocean freight plus surcharges) of the voyages to base ports in US west coast and US east coast were USD 1835/TEU and USD 3056/TEU, respectively down 3.4% and 2.2% from last week. What's worth mentioning is the optimism of US federal reserve board, who predicted the economic growth for 2011 at 3.4% ~ 3.9%, up by 0.4% compared to the figure previously announced in 2010 November. Should the over-estimated growth come real, the prosperity of North America service will be greatly driven forward.

In Singapore and Australia service the cargo volume preserved the downward trajectory as the slot utilization hold below 50%. On February 18th, the freight rate (ocean freight plus surcharges) to the base ports in Australia and Singapore services saw USD 820/TEU, slid 4.5% from last week. With the significant amount of fleet deployed last year, the glut of capacity hardly changed although carriers had put efforts to ameliorate the situation. Under the current downward pressure of the shipment, carriers are now commonly conservative about the short-term market.

Shipments in Japan service turned thriving, but no stronger than half of it was before the holiday. And the freight rate remained hard to rally because of the doom expectations for the next month. On February 18th, the freight index of the Japan service reported 749.37 points, marginally descended from last week.

In Southeast Asia service both the cargo volume and the freight rate slumped, as on February 18th, the freight rate (ocean freight plus surcharges) from Shanghai to Southeast Asia showed USD 149/TEU, down 2.6% from last week. Latest statistics in January from China customs informed that the bilateral trade with ASEAN Free Trade Area has outdo that of with Japan and became the third greatest trading partner for China. Thanks to the sound establishment of ASEAN Free Trade Area, the rapid growing strength of the shipment on the Southeast Asia services would be regarded as one of the most powerful engine for the China's transport market when most western services appeared stagnant.

No hay comentarios:

Publicar un comentario