(CCFI Commentary in Issue 07, 2011)

This week, the China containerized transport market turned gloomy under the post-Chinese lunar new year, as both cargo volume and freight rates shrunk apparently in most main services.

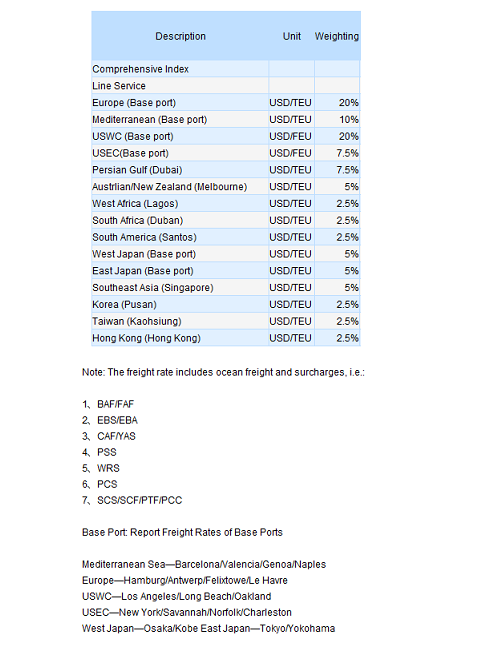

On February 11th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1051.14 points, down 0.8% from last week; while the Shanghai Containerized Freight Index came out at 1091.33 points, down 1.2% from last week.

In Europe service, cargo volume fell drastically comparing to the period before the lunar new year, but with the support of the carrier’s capacity readjustment the slot utilization maintained at 85% while the freight rate descended a little.

On February 11th, the freight index of the Europe service issued by SSE reported 1453.65 points, down 1.3% from last week.

Pundits believed the downward trajectory of the general market hardly changed since it was still in its slack season, but an upsurging momentum is expected to rise after Arpil according to the empirical evidence, which would probably buoyed the container market.

In North America services the sharp decrease in cargo volume this week pulled down the slot utilization to about 80%. And the current sluggish market was mainly shaped by two reasons, first of which is the substantially slumped shipment caused by most manufacturers’ shutdown during the lunar new year; while the second is that the shipment rush ahead of the holiday had fore-delivered part of the cargos in this week, leaving carriers no choice but declining freight rate for solicitation.

On February 11th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in US west coast and US east coast quoted USD 1900/FEU and USD 3124/FEU, respectively down 1.7% and 1.3%.

The cargo volume had greatly contracted on the Australia service after the holiday whereas the freight rate slightly slid a little. While the impact from the flood eased gradually, carriers have been stingy with the capacity since late January, however, the fact of the prevailing slack season and the abundant stockpile had significantly depress the import, lowering the demand of capacity as consequence.

On February 11th, the freight rate (ocean freight plus surcharges) of the voyages to the base ports in Australia and Singapore services saw USD 859/TEU, down 1% from last week.

In Japan service, the slot utilization dropped terribly to less than 50%, while the freight rate maintained steady.

On February 11th, the freight index of the Japan service was 764.68 points, barely changed from last week.

Latest statistics from Japan’s Ministry of Finance showed that the total trade between Japan and China has reached 26.5 trillion yen, up 22.3% from last year, almost returning to the record high before the crisis.

No hay comentarios:

Publicar un comentario