Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 11, 2011)

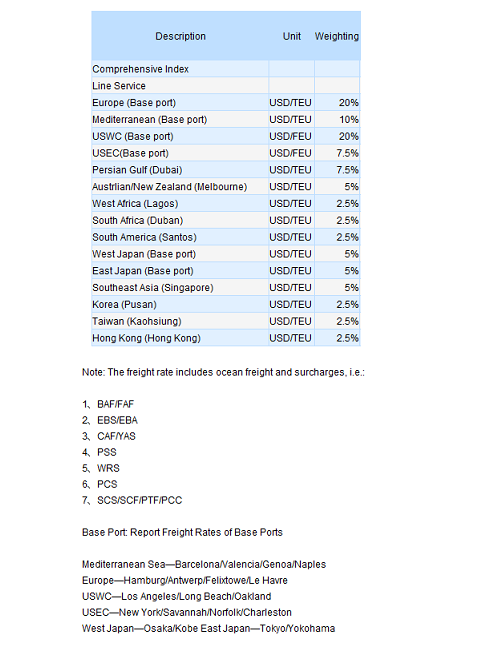

This week, the China containerized transport market marginally went down, with weak demands and freight rates continued in most of the services. On March 11th, the China Containerized Freight Index Issued by Shanghai Shipping Exchange came out at 1027.90 points; while the Shanghai Containerized Freight Index broke through 1000 points threshold to the 993.99 points, down 2.9% from last week.

In Europe and Mediterranean services the inadequate demand, as well as the overcapacity, were still pulling down the freight rate, as on March 11th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Europe and Mediterranean quoted USD 1076/TEU and USD 1042/TEU, respectively down 22% and 15% comparing to the early of the year. Insiders indicated that the slumping freight rate since this year had almost turned the profits generated from the rate restorations in last year to be “vain”. Meanwhile, jumped to the 29 months high, the bunker price had rendered a significant impact on the carriers’ operating cost according to the latest statistics from Alphaliner. So how would the freight rate perform next basically determine the income of the carriers in the 1st quarter.

The capacity demand was still proved slack in North America service, where the slot utilization remain at 70% and the freight rate kept sliding. On March 11th, the freight rates for the voyages to the US west coast and US east coast were USD 1654/FEU and USD 2862/FEU, respectively shrunk by 4.8% and 3.2% from last week.

Volume appeared to rebound on the Australia and Singapore services, as the slot utilization soared to about 75%, while some even showed 80%. Still, the capacity surplus left unchanged, and the freight rate dropped to USD 700/TEU, some of the voyages even saw it below USD 650/TEU. On March 11th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in Australia and Singapore showed USD 745/TEU, down 3.6% from last week. Pundits believe not only the low production caused by the post-lunar new year softened the cargo volume, but the extreme stagnancy of the residents’ spending will in Australia, where the Consumer Confidence Index in March was reported to fall by 2.4% from previous month, resulting an abundant retailing stockpile and the decreasing order for the China’s manufacturers.

In Persian Gulf service, some of the ships were hard to remain unscathed as the rampant Somali piracy frequently occurred in Fareast, Persian Gulf, and the Red Sea, adding up carriers’ risk and cost. Thanks to these pirates, carriers were poised to impose a WRS (Wars Risks Surcharge), pricing at USD 40/TEU. On March 11th, the freight rate of the voyages to the Persian Gulf service reflected USD 726/TEU.

The skyward international oil price forced carriers to speculate on the Bunker Surcharges. Those running on the Southeast Asia services were reported to have implemented an EBS (Emergency Bunker Surcharge) already in this month, quoting about RMB 900/TEU; while the carriers on the North America services introduced Bunker Surcharges of USD 100/FEU in US west coast and USD 200/FEU in US east coast. Also, freight rate over Africa service and South America service were uplifted as well.

No hay comentarios:

Publicar un comentario