Weekly Report of China Export Container Transport Market

This week, a marginal fluctuation turn up in the China containerized transport market, with no obvious swelling in general cargo volume. On March 25th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 1018.25 points; while the Shanghai Containerized Freight Index came out at 989.43 points, basically no change with last week.

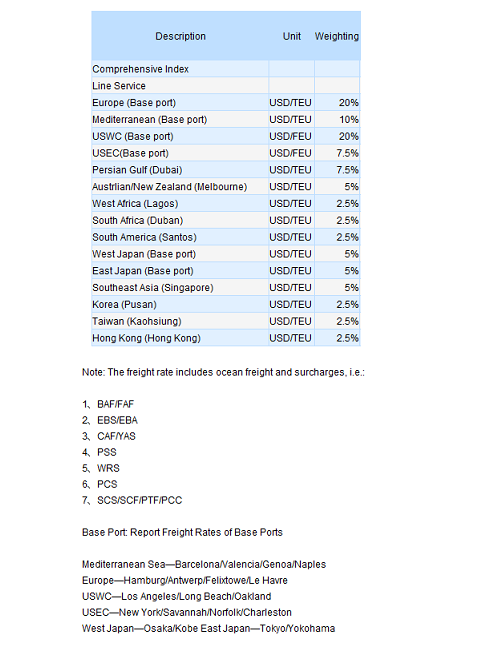

In Europe and Mediterranean service, the volume kept up with previous week, where the slot utilization maintained at 90%. Nevertheless, the massive new-deployed capacity lowered the freight rate, as on March 25th, the freight indices of the Europe and Mediterranean services issued by SSE reported 1320.40 points and 1317.51 points, respectively down 3.4% and 2.3% from last week. Insiders indicated that more fleets would be arranged in the service in April, so the rally is very likely be restrained if the demand couldn't maintained the current upward momentum.

In North America service, the cargo volume kept the trend in last week, and the average slot utilization reported at about 70%. Freight rate was slightly volatile. On March 25th, the freight rate (ocean freight plus surcharges) for the voyages from Shanghai to base ports in US west coast and US east coast were USD 1608/FEU and USD 2819/FEU, basically equaling to last week. The conventional peak season on the North America service in 2nd quarter is approaching, while the rate restoration plans are approaching as well. However, pundits were afraid of the huge tonnage carriers were poised to release, so the glut of capacity, as a result, in the future could put the implement force of the restoration plans into doubt, despite the strong recovery of US' economy.

In Australia and Singapore services, carriers had been cutting 20% of the total capacity since February, where the pressure of capacity surplus was relieved. Besides, the upsurging demand warmed up the slot utilization to about 80%, and the freight rate marginally fluctuated. On March 25th, the freight rate index for the voyages from Shanghai to Australia and Singapore services was 954.95 points, down 0.7% from last week.

In Japan service, the demand ascended a little. The power brownouts over the Japan and the insufficient fuel continued hampering the port operations and the inland box transports. Carriers had already imposed a PCS (Port Congestion Surcharge) for some of the voyages from Shanghai to Kanto, buoying the freight rate. On March 25th, the freight rate index of the Japan service reported 785.56 points, soared 3.1% from last week.

The USDX fell to the yearlow this week, and such slump triggered a boosting crude oil price, to which the Libya woes had contributed as well. Some believe the crude oil price will stay high for a long time. Consequently, not only would the bunker price inflate but also the recovery in most developed countries to be stagnated. And whether the growth of China export containerized market will boom steadily remains to be seen.

No hay comentarios:

Publicar un comentario