Weekly Report of China Export Container Transport Market

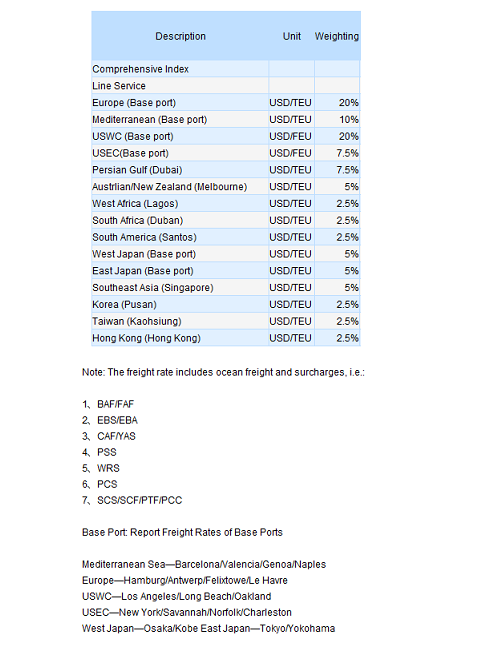

This week, the China’s containerized transport market plunged slightly, while the comprehensive index decreased as well.

On July 15th, the China Containerized Freight Index issued by Shanghai Shipping Exchange was 983.84 points, down 0.5% from last week; while the Shanghai Containerized Freight Index came out at 1016.87 points, down 1.3% from last week.

In Europe service, the market carried on the trend of last week as the slot utilization stayed above 90%. But because of the ongoing capacity glut and the sliding freight rate, the service was regard less prosperous than it was a year earlier. On July 15th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Europe quoted USD 809/TEU, down 1% from last week. Some carriers were said to announce a peak season surcharge in August, but the plan seemed hard to implement because of the surplus fleet. While in Mediterranean the cargo volume tumbled marginally, causing a week-on-week descent over the slot utilization, which is about 90% currently. On July 15th, the freight rate (ocean freight plus surcharges) of the voyages to the base ports in Mediterranean showed USD 926/TEU, down 1.6% from last week.

In North America service this week the cargo volume kept at a high level as there’s a 95% slot utilization in US east coast, where some vessels running out of slots; while the US west coast service behaved not bad as well. Since the amount of fleet didn’t swung much, freight rate barely changed. On July 15th, the freight indices of the US west coast and US east coast services were 947.93 points and 1194.57 points, both grossly equaling to last week. The jobless rate of US had been reported soaring for 3 consecutive months to 9.2%, which would conceivably weaken not only its resident’s purchasing power but also the willingness, with a further impact over the procurement demand during this peak season. Besides, people could also conclude a pessimistic attitude from the carriers given the postponement of the PPS originally planned to impose on July 15th to after August 1st.

In Japan service there wasn’t much change over the cargo volume, where the slot utilization hovered at 70%. Freight rate maintained steadily. On July 15th, the freight index of the Japan service issued by SSE reported 789.06 points, basically the same as last week.

The approaching Ramadan was continuously pushing down the cargo volume exporting to the Persian Gulf with the slot utilization standing at 90%, and freight rate will apparently keep sluggish. It was said that carriers would like to have some surcharge to offset the bearish freight rate, but there’s no indication of when. On July 15th, the freight rate (ocean freight plus surcharges) for the voyages heading to Persian Gulf quoted USD 1005/TEU, down 1.1% from last week.

In Australia and Singapore service the cargo volume was seen firm and the slot utilization reveal at 90%. Freight rate was slightly pushed up by some carriers. Since the market was switching from the slack season to a peak period, cargo volume was estimated to hold still in July and it won’t start rallying until late August. On July 15th, the freight index of the Australia and Singapore service reported 926.73 points, up 1.1% from last week. Owing to the over-deployed capacity, the service proved less profitable than last year.

jueves, 28 de julio de 2011

miércoles, 27 de julio de 2011

Falling freight rates, increasing lay-ups depress charter market prices

THE charter market for containerships is slipping fast in the face of sliding freight rates and increasing lay-ups, according to Alphaliner analysts, which adds that current trends indicate charter rates will fall even more by the end of the year.

Maersk, MSC, CMA CGM continue to be active charterers, but CSAV is re-chartering surplus ships. Alphaliner says CSAV's continuous cutting of services will result in the Chilean carrier removing 100,000 TEU from its slot capacity by the end of August.

Further capacity could be lost if rates continue to fall. The top-four charterers - Maersk, MSC, CMA CGM and CSAV - account for more than 25 per cent of all fixtures. Any slowdown by any of them will have a significant impact on the market, it said.

Because of uncertain market conditions, more charterers are unwilling to sign longer-term deals. This trend is aggravated by the fact that owners have had to accept short charters in an increasingly fragile market as demand weakens.

Both the number of fixtures and the fixture periods have declined significantly since April. Charter rates have dropped by 11 per cent on average in the last three months, with all size segments affected.

Rates are likely to drop in coming months as demand slackens. InJune, the number of reported fixtures reached at the lowest level this year. The average duration of fixtures was cut from 10 months at the beginning of this year to seven months currently.

Maersk, MSC, CMA CGM continue to be active charterers, but CSAV is re-chartering surplus ships. Alphaliner says CSAV's continuous cutting of services will result in the Chilean carrier removing 100,000 TEU from its slot capacity by the end of August.

Further capacity could be lost if rates continue to fall. The top-four charterers - Maersk, MSC, CMA CGM and CSAV - account for more than 25 per cent of all fixtures. Any slowdown by any of them will have a significant impact on the market, it said.

Because of uncertain market conditions, more charterers are unwilling to sign longer-term deals. This trend is aggravated by the fact that owners have had to accept short charters in an increasingly fragile market as demand weakens.

Both the number of fixtures and the fixture periods have declined significantly since April. Charter rates have dropped by 11 per cent on average in the last three months, with all size segments affected.

Rates are likely to drop in coming months as demand slackens. InJune, the number of reported fixtures reached at the lowest level this year. The average duration of fixtures was cut from 10 months at the beginning of this year to seven months currently.

miércoles, 6 de julio de 2011

Capacity growth to reach 8.8% in 2011

Cellular containership capacity is expected to grow by an average annual rate

of 8.7% over the next two years, with 1.26 Mteu due to be added in 2011 and

1.33 Mteu in 2012, based on Alphaliner projections. These figures follow the

1.20 Mteu which have been added to the fleet in 2010. Although the fleet increases

over 2011-2012 will not reach the figures recorded in 2006-2008,

when an average of 1.37 Mteu per year were added, the level of capacity additions

remains a key concern for the industry.

![]()

A large part of the new capacity added in 2010 was absorbed by the increased

demand that was caused by the rapid economic recovery. Throughput volumes

at the world’s five busiest container ports grew by 18% on average in the first

three quarters of 2010. However, the average growth at these ports has slowed

to 8% in the fourth quarter, with the trend towards slower growth likely to persist

into 2011.

The slowing of the demand in the fourth quarter has already started to hurt carriers’

load factors. Alphaliner estimates of vessel utilization levels on the Far

East-US and Far East-Europe routes dropped to only 80% in December, the lowest

levels recorded since May 2009. Attention must now be shifted to utilization

levels in the next two months, as these will determine the direction of

freight rates after the Lunar New Year celebrations in the Far East.

Aphaliner

of 8.7% over the next two years, with 1.26 Mteu due to be added in 2011 and

1.33 Mteu in 2012, based on Alphaliner projections. These figures follow the

1.20 Mteu which have been added to the fleet in 2010. Although the fleet increases

over 2011-2012 will not reach the figures recorded in 2006-2008,

when an average of 1.37 Mteu per year were added, the level of capacity additions

remains a key concern for the industry.

A large part of the new capacity added in 2010 was absorbed by the increased

demand that was caused by the rapid economic recovery. Throughput volumes

at the world’s five busiest container ports grew by 18% on average in the first

three quarters of 2010. However, the average growth at these ports has slowed

to 8% in the fourth quarter, with the trend towards slower growth likely to persist

into 2011.

The slowing of the demand in the fourth quarter has already started to hurt carriers’

load factors. Alphaliner estimates of vessel utilization levels on the Far

East-US and Far East-Europe routes dropped to only 80% in December, the lowest

levels recorded since May 2009. Attention must now be shifted to utilization

levels in the next two months, as these will determine the direction of

freight rates after the Lunar New Year celebrations in the Far East.

Aphaliner

CCFI Commentary Issue 26, 2011

Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 26, 2011)

This week, the China’s containerized transport market was little better, as the comprehensive index was still seen sluggish. On June 24th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 981.65 points, down 1.7% from last week; while the Shanghai Containerized Freight Index came out at 1024.77 points, down 0.6% from last week.

In Europe service, the demand for the capacity maintained an upward momentum, with a 90% slot utilization. Insiders estimated that there would be a drastic boost of the cargo volume on the first week of July, following a slots scarcity in the next one as the arrival of the conventional peak season. Affected by such optimism, the prevailing freight rate somehow tempered its falling trend while some carriers slightly uplift the freight rate. On June 24th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Europe and Mediterranean services were USD 845/TEU and USD 953/TEU, respectively down 0.5% and 0.2% from last week. The current freight rate on the service was reported staying below the breakeven point, so some carriers would shut off some routes if the freight rate kept dipping.

The North America service seemed bearish this week, and the cargo volume was still depressing as last week. Slot utilizations in US west and US east reported only 80% and 90% respectively. Since the service became less profitable, some carriers had already announced to suspend their voyages. The continuously descending freight rate had mostly nullified the conventional peak season, leaving some carriers delaying the PSS plan till mid-June. On June 24th, the freight indices of the US west and US east coast services issued by SSE were 938.48 points and 1174.13 points, respectively tumbled by 2.3% and 0.6% from last week. Pundits indicated that several carriers like Hanjin and APL would adopted a new formula to account the BAF in 3rd quarter, which will probably cut the existing one, published by the TSA on the US west and US east coast services, by USD 30/TEU and USD 48/TEU. Besides, carriers are expecting a shipment rally when mid-June and consequently kicks up the freight rate.

In Japan service this week the slot utilization climbed up to 70%. Moreover, the port congestions occurred a few weeks ago had been just relieved, resuming the shipping schedule of most voyages. On June 24th, the freight index of the Japan service issued by SSE reported 789.25 points. After the abolition of the emergency cost surcharge of Shanghai on June 1st, ports of northern China were said to go with the flow on August 1st. Relevant news might be released in the next few weeks.

In Persian Gulf service this week the cargo volume saw flat with a slot utilization of 85%. The Ramadan over the middle-east region started on August 1st and will possibly pressure the cargo volume in mid-July. Meanwhile, inflicted by the poor Europe service, the freight rate was perceived steadily decreasing. On June 24th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to Persian Gulf quoted USD 1014/TEU, down 0.5% from last week.

In Australia and Singapore service the cargo volume hardly changed, with the slot utilization hovering from 80% to 85%. Pundits believed that the freight rate won’t stop dropping until mid-July. On June 24th, the freight index of the Australia and Singapore service reported 934.51 points, down 1.1% from last week.

(CCFI Commentary in Issue 26, 2011)

This week, the China’s containerized transport market was little better, as the comprehensive index was still seen sluggish. On June 24th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 981.65 points, down 1.7% from last week; while the Shanghai Containerized Freight Index came out at 1024.77 points, down 0.6% from last week.

In Europe service, the demand for the capacity maintained an upward momentum, with a 90% slot utilization. Insiders estimated that there would be a drastic boost of the cargo volume on the first week of July, following a slots scarcity in the next one as the arrival of the conventional peak season. Affected by such optimism, the prevailing freight rate somehow tempered its falling trend while some carriers slightly uplift the freight rate. On June 24th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Europe and Mediterranean services were USD 845/TEU and USD 953/TEU, respectively down 0.5% and 0.2% from last week. The current freight rate on the service was reported staying below the breakeven point, so some carriers would shut off some routes if the freight rate kept dipping.

The North America service seemed bearish this week, and the cargo volume was still depressing as last week. Slot utilizations in US west and US east reported only 80% and 90% respectively. Since the service became less profitable, some carriers had already announced to suspend their voyages. The continuously descending freight rate had mostly nullified the conventional peak season, leaving some carriers delaying the PSS plan till mid-June. On June 24th, the freight indices of the US west and US east coast services issued by SSE were 938.48 points and 1174.13 points, respectively tumbled by 2.3% and 0.6% from last week. Pundits indicated that several carriers like Hanjin and APL would adopted a new formula to account the BAF in 3rd quarter, which will probably cut the existing one, published by the TSA on the US west and US east coast services, by USD 30/TEU and USD 48/TEU. Besides, carriers are expecting a shipment rally when mid-June and consequently kicks up the freight rate.

In Japan service this week the slot utilization climbed up to 70%. Moreover, the port congestions occurred a few weeks ago had been just relieved, resuming the shipping schedule of most voyages. On June 24th, the freight index of the Japan service issued by SSE reported 789.25 points. After the abolition of the emergency cost surcharge of Shanghai on June 1st, ports of northern China were said to go with the flow on August 1st. Relevant news might be released in the next few weeks.

In Persian Gulf service this week the cargo volume saw flat with a slot utilization of 85%. The Ramadan over the middle-east region started on August 1st and will possibly pressure the cargo volume in mid-July. Meanwhile, inflicted by the poor Europe service, the freight rate was perceived steadily decreasing. On June 24th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to Persian Gulf quoted USD 1014/TEU, down 0.5% from last week.

In Australia and Singapore service the cargo volume hardly changed, with the slot utilization hovering from 80% to 85%. Pundits believed that the freight rate won’t stop dropping until mid-July. On June 24th, the freight index of the Australia and Singapore service reported 934.51 points, down 1.1% from last week.

Suscribirse a:

Comentarios (Atom)