Weekly Report of China Export Container Transport Market

This week, the China’s containerized transport market plunged slightly, while the comprehensive index decreased as well.

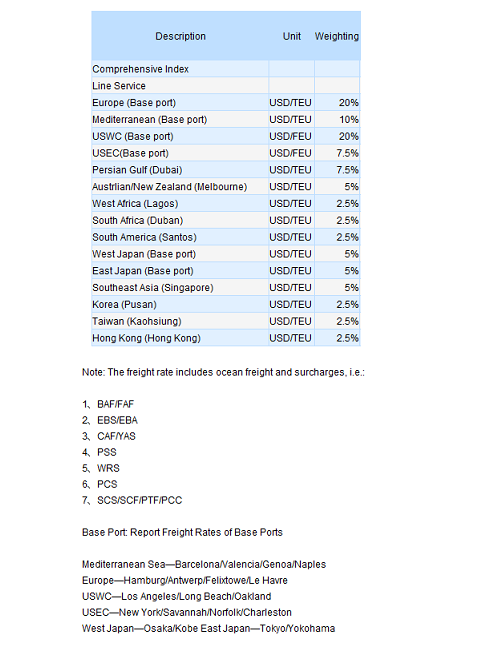

On July 15th, the China Containerized Freight Index issued by Shanghai Shipping Exchange was 983.84 points, down 0.5% from last week; while the Shanghai Containerized Freight Index came out at 1016.87 points, down 1.3% from last week.

In Europe service, the market carried on the trend of last week as the slot utilization stayed above 90%. But because of the ongoing capacity glut and the sliding freight rate, the service was regard less prosperous than it was a year earlier. On July 15th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Europe quoted USD 809/TEU, down 1% from last week. Some carriers were said to announce a peak season surcharge in August, but the plan seemed hard to implement because of the surplus fleet. While in Mediterranean the cargo volume tumbled marginally, causing a week-on-week descent over the slot utilization, which is about 90% currently. On July 15th, the freight rate (ocean freight plus surcharges) of the voyages to the base ports in Mediterranean showed USD 926/TEU, down 1.6% from last week.

In North America service this week the cargo volume kept at a high level as there’s a 95% slot utilization in US east coast, where some vessels running out of slots; while the US west coast service behaved not bad as well. Since the amount of fleet didn’t swung much, freight rate barely changed. On July 15th, the freight indices of the US west coast and US east coast services were 947.93 points and 1194.57 points, both grossly equaling to last week. The jobless rate of US had been reported soaring for 3 consecutive months to 9.2%, which would conceivably weaken not only its resident’s purchasing power but also the willingness, with a further impact over the procurement demand during this peak season. Besides, people could also conclude a pessimistic attitude from the carriers given the postponement of the PPS originally planned to impose on July 15th to after August 1st.

In Japan service there wasn’t much change over the cargo volume, where the slot utilization hovered at 70%. Freight rate maintained steadily. On July 15th, the freight index of the Japan service issued by SSE reported 789.06 points, basically the same as last week.

The approaching Ramadan was continuously pushing down the cargo volume exporting to the Persian Gulf with the slot utilization standing at 90%, and freight rate will apparently keep sluggish. It was said that carriers would like to have some surcharge to offset the bearish freight rate, but there’s no indication of when. On July 15th, the freight rate (ocean freight plus surcharges) for the voyages heading to Persian Gulf quoted USD 1005/TEU, down 1.1% from last week.

In Australia and Singapore service the cargo volume was seen firm and the slot utilization reveal at 90%. Freight rate was slightly pushed up by some carriers. Since the market was switching from the slack season to a peak period, cargo volume was estimated to hold still in July and it won’t start rallying until late August. On July 15th, the freight index of the Australia and Singapore service reported 926.73 points, up 1.1% from last week. Owing to the over-deployed capacity, the service proved less profitable than last year.

No hay comentarios:

Publicar un comentario