Weekly Report of China Export Container Transport Market(CCFI Commentary in Issue 33, 2011)

This week, the China’s containerized transport market maintained firm, with the composite index slightly increased. On August 12th, the China Containerized Freight Index issued by Shanghai Shipping Exchange was 983.52 points, up 0.5% from last week; while the Shanghai Containerized Freight Index came out at 1033.24 points, up 1.4% from last week.

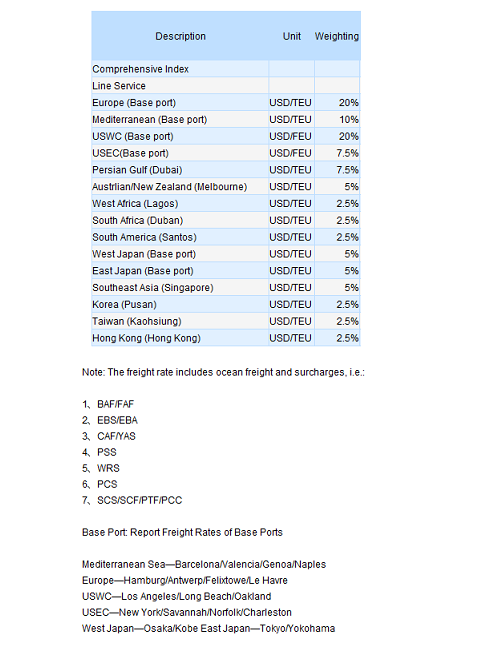

In Europe service this week, the cargo volume hiked steadily, buoying the slot utilization up to above 90% with some voyages running out of slots. The thriving market quotation stabilized the freight rate after its previous upturn, while in some voyages the price continued went up with the upward trajectory of last week. On August 12th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Europe service reported USD 828/TEU, up 0.6% from last week. In Mediterranean service, the ongoing conventional peak season stimulated the slot utilization to above 95%, with the freight rates over the west Mediterranean voyages climbed up to USD 1050/TEU. On August 12th, the freight rate (including ocean freight and surcharges) of the voyages to Mediterranean service was USD 1019/TEU, up 5.5% from last week.

In North America, a sharp differential turned up between the west- and east-bound services. In US west coast service the cargo remained sluggish and the slot utilization stood at about 85%. Freight rate kept dipping, while for some voyages the price had even fallen to USD 1300/FEU, which is near half of what it was a year earlier. On August 12th, the freight index of the US west coast service reported 903.59 points, down 1.7% from last week. The US east coast service was seen bullish, giving the limited capacity influx, sound supply-demand relation, and a 95% slot utilization, which in some cases it was 100%. On August 12th, the freight index of the US east coast service was 1191.18 points, basically equaling to last week. Thanks to the coming conventional peak season, carriers were poised to announce a USD 400/FEU peak season surcharge since August 15th. However, people were afraid of the plan’s implementation as the weak cargo volume and the excessive capacity could not be ignored. As a result, some were reported delaying the announcement to 22nd and cutting the price added.

However, whether the implementation will be fulfilled was conceived as an uncertainty by the market citing the weak cargo volume and the excessive capacity.

In Australia and Singapore service, the approaching conventional peak season left the cargo volume in a strong upward momentum, where the slot utilization hovering above 95% and more voyages were reported laden. Freight rate kept ascending because of the improved supply-demand relations. On August 12th, the freight rate (ocean freight plus surcharges) of the Australia and Singapore service appeared USD 833/TEU, burst by 16.7% from last week. Considering the outstanding performance of the cargo volume, carriers tended to uplift the freight rate once again by about USD 200/TEUl.

In Persian Gulf service, inflicting by the Ramadan, the cargo volume kept slipping and the slot utilization revealed at 90%. Freight rate kept the slumping behavior of last week. On August 12th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Persian Gulf service quoted USD 953/TEU, down 0.7% from last week. As the demand of the capacity generally restrained, some carriers would cut their capacity by switching small tonnages into larger ones.

No hay comentarios:

Publicar un comentario