Weekly Report of China Export Container Transport Market

(CCFI Commentary in Issue 26, 2011)

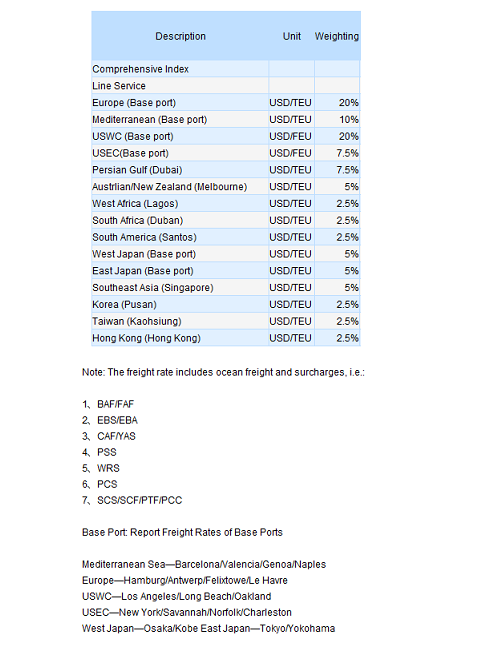

This week, the China’s containerized transport market was little better, as the comprehensive index was still seen sluggish. On June 24th, the China Containerized Freight Index issued by Shanghai Shipping Exchange reported 981.65 points, down 1.7% from last week; while the Shanghai Containerized Freight Index came out at 1024.77 points, down 0.6% from last week.

In Europe service, the demand for the capacity maintained an upward momentum, with a 90% slot utilization. Insiders estimated that there would be a drastic boost of the cargo volume on the first week of July, following a slots scarcity in the next one as the arrival of the conventional peak season. Affected by such optimism, the prevailing freight rate somehow tempered its falling trend while some carriers slightly uplift the freight rate. On June 24th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to base ports in Europe and Mediterranean services were USD 845/TEU and USD 953/TEU, respectively down 0.5% and 0.2% from last week. The current freight rate on the service was reported staying below the breakeven point, so some carriers would shut off some routes if the freight rate kept dipping.

The North America service seemed bearish this week, and the cargo volume was still depressing as last week. Slot utilizations in US west and US east reported only 80% and 90% respectively. Since the service became less profitable, some carriers had already announced to suspend their voyages. The continuously descending freight rate had mostly nullified the conventional peak season, leaving some carriers delaying the PSS plan till mid-June. On June 24th, the freight indices of the US west and US east coast services issued by SSE were 938.48 points and 1174.13 points, respectively tumbled by 2.3% and 0.6% from last week. Pundits indicated that several carriers like Hanjin and APL would adopted a new formula to account the BAF in 3rd quarter, which will probably cut the existing one, published by the TSA on the US west and US east coast services, by USD 30/TEU and USD 48/TEU. Besides, carriers are expecting a shipment rally when mid-June and consequently kicks up the freight rate.

In Japan service this week the slot utilization climbed up to 70%. Moreover, the port congestions occurred a few weeks ago had been just relieved, resuming the shipping schedule of most voyages. On June 24th, the freight index of the Japan service issued by SSE reported 789.25 points. After the abolition of the emergency cost surcharge of Shanghai on June 1st, ports of northern China were said to go with the flow on August 1st. Relevant news might be released in the next few weeks.

In Persian Gulf service this week the cargo volume saw flat with a slot utilization of 85%. The Ramadan over the middle-east region started on August 1st and will possibly pressure the cargo volume in mid-July. Meanwhile, inflicted by the poor Europe service, the freight rate was perceived steadily decreasing. On June 24th, the freight rate (ocean freight plus surcharges) of the voyages from Shanghai to Persian Gulf quoted USD 1014/TEU, down 0.5% from last week.

In Australia and Singapore service the cargo volume hardly changed, with the slot utilization hovering from 80% to 85%. Pundits believed that the freight rate won’t stop dropping until mid-July. On June 24th, the freight index of the Australia and Singapore service reported 934.51 points, down 1.1% from last week.

No hay comentarios:

Publicar un comentario